By Andrew Hecht, Seeking Alpha

Summary

- A compromise — an extension.

- ECB is more worried about what is ahead.

- A leftist leader emerges in Spain.

- The Euro is going to parody against the U.S. dollar.

All week the markets waited for news out of Europe — who would fold their hand first, the Greeks or the European Central Bank? Since the Greek election, which was a rejection of the austerity programs leveled by the ECB, the new Greek government has played hardball. As tough as Prime Minister Tsipras and Finance Minister Varoufakis have played, finance ministers from Europe played harder. The news came late Friday; that news was no surprise. It spared Europe a Greek default, for now.

A compromise — an extension

The news, a temporary fix, was Greek capitulation. Both sides took something away from the outcome. A four-month extension bought the Greeks more time. However, the extension is contingent upon Greece submitting to monitoring and an approval by the ECB of proposed economic reforms. The compromise actually put the Greeks in a worse place than they were in before the negotiations. They will now report not only to the ECB, but the European Union and the International Monetary Fund will also monitor them. The bottom line is that Greece caved to the pressure put upon them by the other European finance ministers. In a late-day press conference on Friday, Greek finance minister Varoufakis put a positive spin on the outcome, saying the Greeks are now “co-authors” of their economic destiny. Four months will pass by very quickly and the Greeks will be right back in the same position in late June. That is, of course, if the ECB gives a thumbs up on Greek proposed reforms this coming Monday. Whatever happens, it seems likely that the Greeks will eventually need another bailout but for now, the country will remain inside the euro. The ECB played hardball — other issues will come up in 2015 and the last thing they wanted was to set a precedent they might regret later.

ECB is more worried about what is ahead

The ECB had to bail out other southern European nations over recent years. The economies in these countries continue to suffer. Deflationary pressures and rising unemployment have also plagued countries like Spain, Italy and Portugal while growth has been non-existent. The Greek election was a popular rejection of austerity. Over the course of coming months these other nations will hold elections. As the citizenry suffers, it is likely that current governments will be defeated in elections. A new Greek government is an example to the rest of Europe, and it is something that sends shivers down the spines of many of the Northern European leaders and policy makers sitting in Brussels and the ECB in Frankfurt.

A leftist leader emerges in Spain

Spain will go to the polls on or before December 20, 2015. Currently an anti-establishment, anti-austerity party called Podemos is leading in the polls. Podemos means “we can.” The leader of the party is a 36-year-old with a doctorate in political science and a masters degree in communication. Pablo Iglesias is a plain-speaking charismatic figure who despite his youth seems destined to take power. He is appealing to the Spanish electorate with promises of a higher minimum wage and a shorter working week. His policies are a clear rejection of European austerity. The ECB looks like it is going to have its hands full in the months ahead. The Greeks led by Tsipras and Varoufakis and now the potential of a leftist leader in Spain will cause Northern European leaders to lose lots of sleep in coming months. Physics teaches that for every action, there is an equal and opposite reaction. The reaction to slow growth, unemployment and austerity in Southern Europe is a new breed of young, fiery and charismatic leaders. The melding of cultures is certainly playing out in an interesting way and it is probable that we have not seen anything yet.

All of these prospects will translate into increasing volatility for the euro currency. The policy of quantitative easing instituted by the ECB in January will keep interest rates low in hopes of stimulating the European economies. However, time and patience is running out in the countries where economic hardship is the greatest. Global deflationary pressures, sanctions on Russia and immigration problems in Europe continue to plague the continent.

The Euro is going to parity against the U.S. dollar

While Europe is lowering interest rates and suffering economic contraction, the U.S. economy continues to do well on a relative basis. The U.S. Federal Reserve released minutes from its January meeting this week. Those minutes revealed that Fed Governors are wary of raising short-term interest rates given the strength of the dollar. The Fed is stuck in a difficult situation. They said that they would raise rates in 2015 last year. However, now they are retreating. Whether or not the Fed does in fact raise rates, even symbolically, may not matter as the market may take care of that for them. This past week signs that rates are likely to rise came from the markets. Interest sensitive stocks showed some weakness. The thirty-year U.S. Treasury bond futures market has moved from 151 28/32 on January 30 to close on Friday, February 20 at 144 14/32. The iShares 20+ Year Treasury Bond ETF (NYSEARCA:TLT) has moved from $138.28 on January 30 to $126.54 on Friday. Higher interest rates in the United States will turbo-charge the dollar. The fundamentals already favor a higher U.S. currency against the euro given the political and economic landscapes. Higher U.S. interest rates will just make an already strong case for the dollar even stronger. Investors will receive even more interest to wait for the capital appreciation that seems almost certain these days. All the while, European interest rates are at zero or lower.

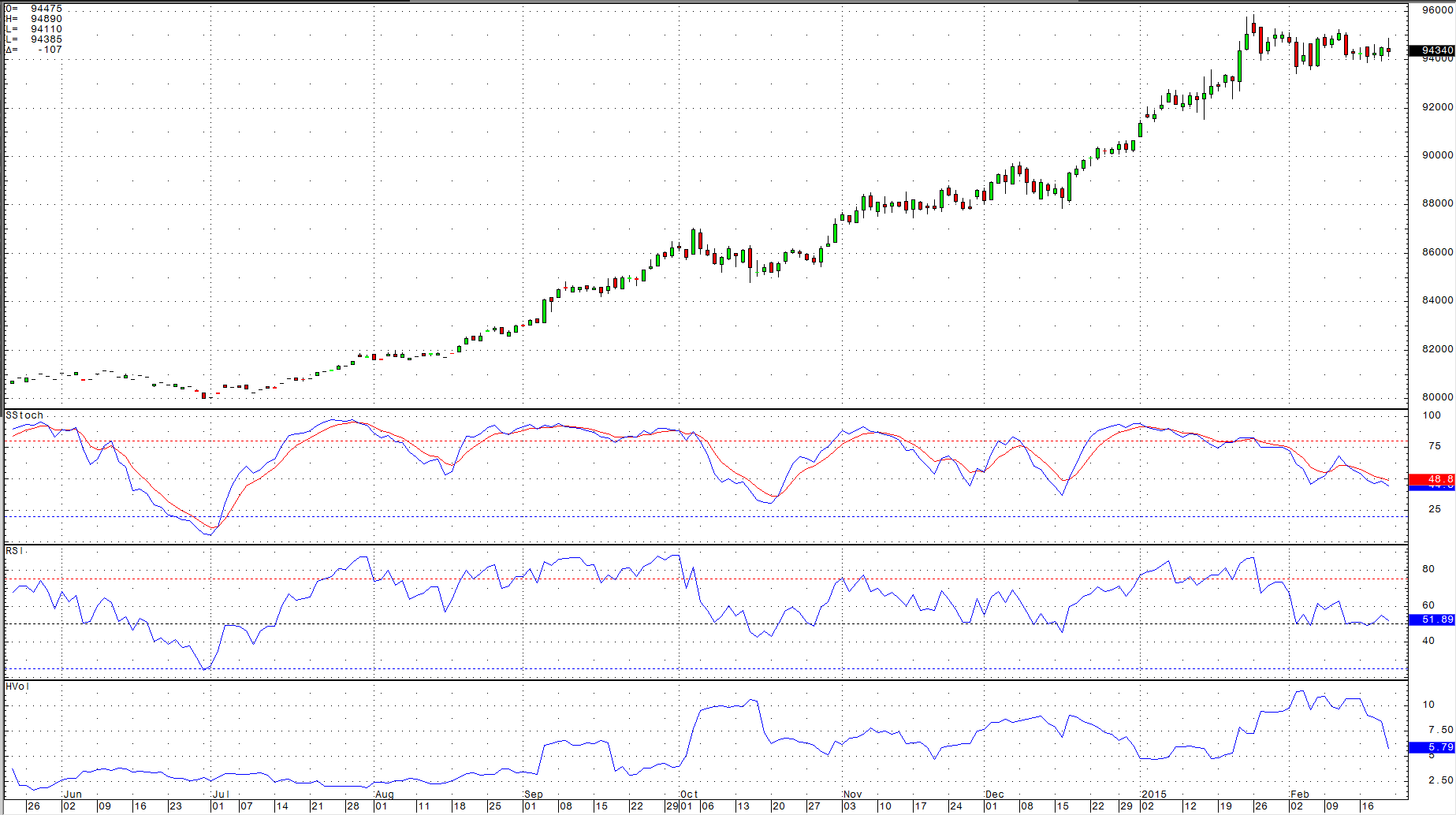

Meanwhile the dollar had a sideways week. Even in the face of a compromise with Greece, the euro could not stage a rally. For now, the upward trajectory of the dollar has slowed. (click to enlarge)

The chart of the daily action in the U.S. dollar index illustrates that it is currently going through a period of consolidation. Overbought conditions are being relieved and historical volatility is dropping. This is not a negative for the dollar, which has rallied for nine straight months. Rather, given the compromise announced Friday with the Greeks, the dollar gave up little ground.

The technical picture for the dollar and the fundamentals that underpin the greenback versus the euro continue to scream that the dollar is going to parity. This may happen sooner rather than later. Meanwhile, political change in economically suffering European countries is likely in 2015. Greece led the way and they are a thorn in the northern countries’ side; other thorns will emerge after elections. I wonder whether conjecture about Greece and other southern countries exiting the euro will eventually shift to a fed-up north. Finance ministers and leaders in Germany and other northern member nations continue to hold the southern countries’ feet to the fire. Perhaps the Germans will eventually give up and go back to a single economic system. Wouldn’t that be a twist of fate?

{kind=link}