How the smart money is approaching the latest drama

CONTRARIAN investors love terrifying headlines. The more unloved the country, the more undervalued its assets and the more money to be made as its fortunes turn. Moneymen who shrewdly exploited the on-again-off-again panic regarding Greece’s finances have made handsome profits in recent years.

In the second half of 2012, for instance, holders of Greek government bonds doubled their money. In the second half of 2013 the main stockmarket index rose by almost 40%. It is striking, therefore, how hard it is these days to find financiers willing to make any bets on Greece at all.

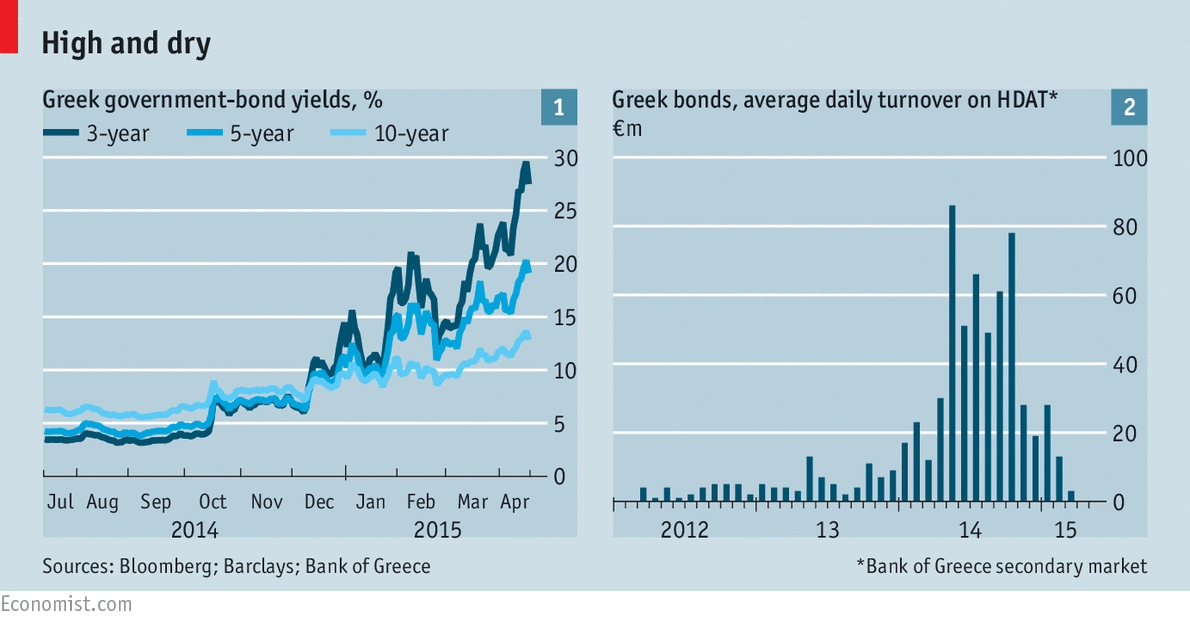

The country is once again running out of money. On April 24th euro-zone finance ministers are due to meet in Latvia to decide whether to provide a lifeline by disbursing the last instalment of the existing bail-out package. The problem is that Greece’s new government has refused to implement reforms promised by its predecessor, and has not proposed alternatives its creditors consider adequate. Talks continue, but the two sides remain far apart. If Greece does not secure more cash, it will soon have to default either on its own citizens (see Free exchange) or on the IMF and the European Central Bank (ECB). That, in turn, could prompt the ECB to withhold support for Greek banks, forcing Greece to impose capital controls and perhaps to withdraw from the euro.All manner of financial indicators suggest disaster is imminent. The Greek government’s three-year bonds now yield a dizzying 27%. Ten-year government bonds are trading at their highest yields (and therefore lowest prices) since 2012 (see chart 1). Credit-default swaps, which offer insurance against a default, suggest an 80% chance of one within five years. Listed Greek firms are trading at less than 60% of their book value, on average. Greek bank stocks are down by 75% compared to this time last year.

Betting house Paddy Power puts the odds of Greece adopting a new currency before 2018 at 5/4, of a new election being held this year at 3/1 and of Greece exiting the euro zone this year at 2/1. William Hill, another bookmaker, has stopped taking bets on “Grexit” altogether because too many people are putting their money on it. Just in case anyone still thought Greek debt was a sound investment, S&P, a rating agency, downgraded it to a lower category of junk earlier this month.

All of which marks a change. In recent years Greece had seemed like the ideal destination for contrarian investors: in enough trouble that assets were cheap, but with the near-certainty that Europe would bail it out. In 2012 and 2013 hedge funds such as Third Point and Alden, among others, began hastily drumming up money to bet on a Greek recovery. Others followed in 2014 as foreigners ploughed more money than expected into local banks. John Paulson, who runs a feted hedge fund, was among those buying shares. Last April, when Greece returned to the international market to sell five-year bonds, yield-hungry investors piled in. Even when Syriza came to power in January and markets wobbled, a few opportunistic investors increased their positions, convinced the difficulties would be temporary.

Today few foreigners remain and most of those have trimmed their positions. After two bail-outs, only 11% of Greece’s government bonds are in private hands. Eaglevale, an American hedge fund whose Greek investments lost half their value last year, is now abandoning the bond market. After a flurry of interest in the run-up to the election in January, trading has atrophied (see chart 2).

Analysts at big banks still hope for a compromise but concede that the odds are lengthening. A few investors, such as Japonica, another American hedge fund, are still convinced they will be vindicated, but most are hedging their bets (for example, by shorting Greek stocks) or are simply stuck because it is hard to sell in such an illiquid market. Some, like Mr Paulson, whose shares in Piraeus Bank are now worth a fifth of what he paid, are staying put and hoping for the best. But nearly all agree that their investments will prove either a bonanza or a wipeout. “Although compromise is still the most likely outcome, many Greek stocks and all of the banks are either trading violently cheap or are worth more or less zero,” argues Matthew Wood of Lancaster Investment Managers.

Most moneymen, however, are studying events in Greece not with a view to investing there, but to gauge the impact elsewhere. Government-bond yields remain subdued in other cash-strapped Mediterranean countries, but pessimists attribute that more to the ECB’s big bond-buying scheme than to confidence in places such as Italy and Portugal. Francesco Garzarelli of Goldman Sachs, an investment bank, says contagion will be greater if Greece’s euro-zone peers eject it from the currency union by inducing the ECB to withhold emergency funding from its banks, as that would fundamentally alter investors’ grasp of how the euro zone works. Yanis Varoufakis, Greece’s finance minister, this week cautioned, “Anyone who says they know what will happen if Greece is pushed out of the euro is deluded.”

Optimists argue that the euro zone is much better able to absorb a Greek shock today than it was in 2011. Banks are better capitalised and have virtually no exposure to Greece; quantitative easing is propping up bond and equity markets; and thanks to the weak euro, exports are much stronger. Many investors think volatility will be temporary, with stocks and bonds dropping before rebounding. If Greece defaults and people start selling off European stocks, just buy more, reckons Philippe Jabre, a veteran hedge-fund manager. “If we’re wrong, it’s an easy market to exit. If we’re right, we can make a lot of money.”

Some even argue that Grexit would do markets good by frightening other countries into accelerating reforms, reducing support for protest parties such as Podemos in Spain and giving twitchy investors the confidence that the euro zone can weather such a crisis. The contagion to worry about, Mr Jabre reckons, would come from Europe caving in to Greek recalcitrance, giving other countries an incentive to follow suit.

{kind=link}