By Matt O’Brien, Washington Post

Greece’s economic crisis is over only if you don’t live there.

Everyone else, in other words, might have moved on because Greece isn’t threatening to knock over the other dominoes that are known as the global economy anymore, but its people are still stuck in what is the worst collapse a rich country has ever gone through. Indeed, if the International Monetary Fund’s latest projections are correct, it might be at least another 10 years before Greece is back to where it was in 2007. And that’s only if there isn’t another recession between now and then.

Two lost decades, then, are something of a best-case scenario for Greece.

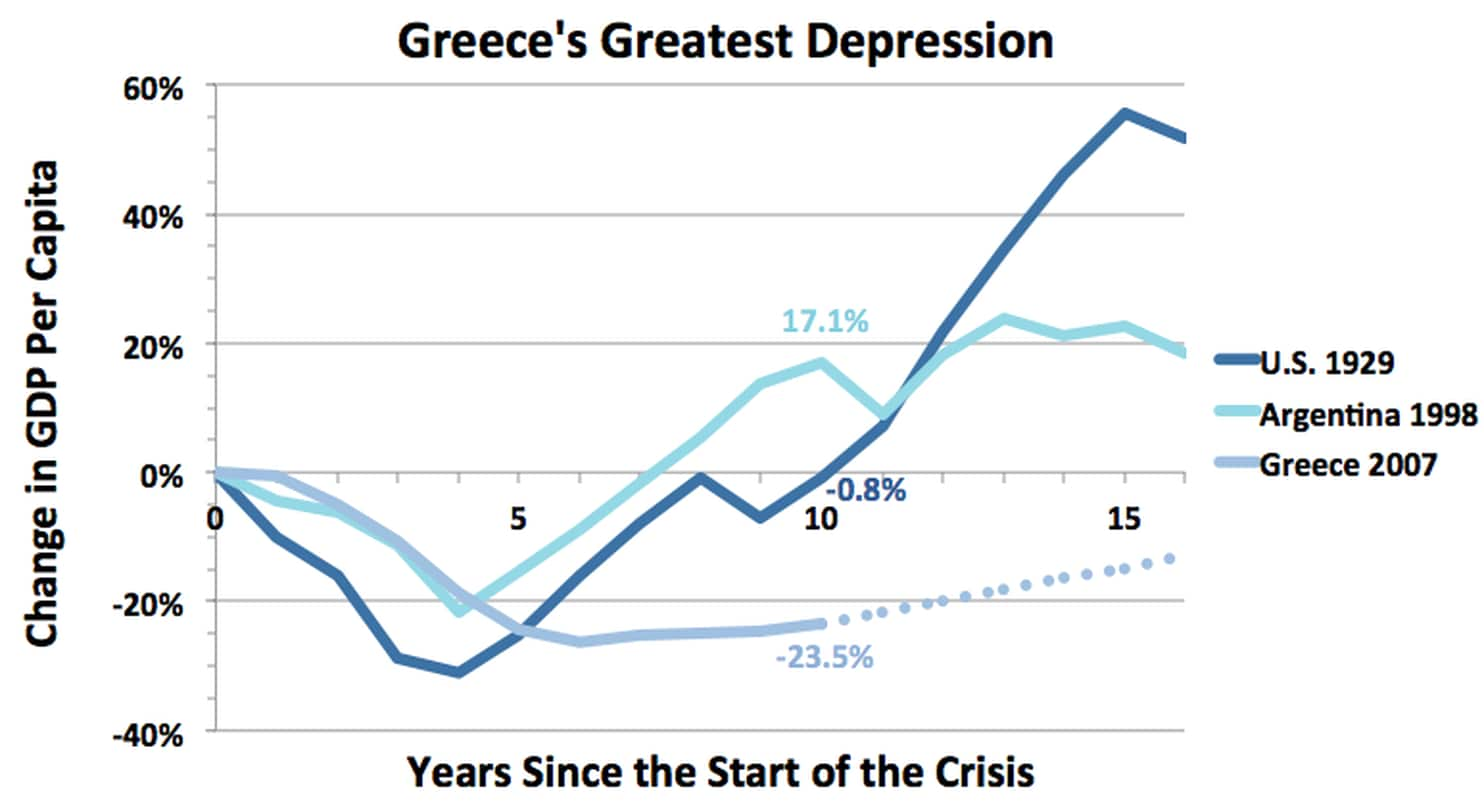

The numbers are staggering. It’s not just that Greece’s economy shrank 26 percent in per capita terms between the middle of 2007 and the start of 2014. That, as you can see below, might have put it on par with some of the biggest calamities in economic history — it was a little better than the United States had done in the 1930s, but a little worse than Argentina had done in the 2000s — but it didn’t distinguish it among them. No, it’s that Greece has grown only a total of 2.8 percent — again, adjusted for its population — in the first four years of what is supposedly a recovery. To give you an idea how miserable that is, 1930s America grew 30.2 percent and 2000s Argentina grew 26.9 percent during the first four years of theirs.

The result is that, by this point of their recoveries, the United States was nearly all the way back to where it had been before its crash, and Argentina was actually 17.1 percent richer than it had been. Greece, meanwhile, is still 23.5 percent poorer than it was.

Source: International Monetary Fund; Angus Maddison

There is a simple reason the United States and Argentina got V-shaped recoveries, while Greece is eking out an L-shaped one (which is to say, not one at all). All three countries, you see, had more or less pegged their currencies to something else — the United States to gold, Argentina to the dollar and Greece to the euro. In doing so, the gave up control over their monetary policies. That meant that they could no longer just print money whenever their economies needed it, because they had to worry first and foremost about keeping that money worth as much as whatever they had pegged it to. The value of their currency, not the state of their economy, dictated how much stimulus they got.

So if things went wrong, either because households ran up too much debt, or companies did, or maybe even the government, there wasn’t anything they could do to cushion the blow. Their currency pegs not only stopped them from cutting interest rates as much as they needed to, but also from spending more money to keep the bottom from falling out. The only thing left was to cut wages and hope that that would make them competitive enough to export their way out of trouble. The problem there, though, is that people’s debts don’t go down when their pay does, so what’s supposed to be good for the economy as a whole ends up being bad for every individual in it. It’s a doom loop where more pay cuts lead to more bankruptcies, and more bankruptcies lead to more pay cuts.

The only way out is to give up your peg so you can give your economy whatever stimulus it needs. And, if you take another look, it isn’t hard to tell when the United States and Argentina did so: It was when their recoveries started. What about Greece, though? Well, it still hasn’t. That’s why its economy hasn’t bounced back, even though it has stopped falling. It’s stuck somewhere between a recession and a recovery.

The truth is that there are no easy answers for Greece. It’s true that it would probably be in better shape today if it had defaulted on all its debt and left the euro back in, say, 2009. There would have been even more immediate pain — Greece imports a lot of its food and all of its oil — but it would have made Aegean vacations so cheap that everyone else wouldn’t have been able to afford not to take them, and the country’s exports would have become so much more competitive overnight that it would have gotten them back to growth much, much quicker than they are today.

But, of course, it didn’t do those things, and it’s hard to justify them now. That’s because Greece doesn’t have just a currency peg but a currency union. The simple story is that it’s much more difficult to replace a currency than it is to say that it won’t be worth a certain amount anymore. You have to substitute all the money in the banks, which probably means shutting them down until you do, and, in the meantime, the resulting panic will send the economy spiraling down once again. That’s a big part of the reason Greece hasn’t left the euro. The fact that its people still think of it as both the imprimatur and guarantor of economic success is the other — and it’s not going to change.

Neither, it seems, is Greece’s slow recovery. The IMF somewhat optimistically thinks that Greece will still be 12.8 percent poorer than it was in 2007 in 2023, which would put it on pace to get back to its pre-recession peak sometime around 2030 or so.

They have made a desert, and called it a recovery.