By Dean Popplewell, Forbes

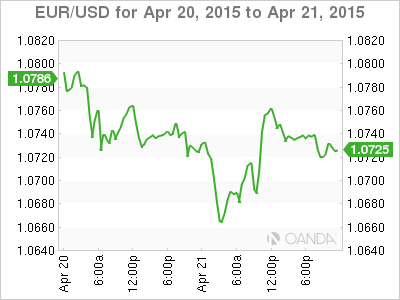

The U.S. dollar edged up against several other currencies on Tuesday, supported by a euro that’s under increasing pressure due to the Greek imbroglio.

Investors will find themselves in a tough spot seeking direction in a week that’s deprived of fundamental data and long on Greece surviving as a eurozone member.

The markets are wary that elevated Greek uncertainty is to persist as the country’s problems are on the verge of worsening. It’s why investors remain cautious about Friday’s Eurogroup meeting to see if Greece will actually deliver on any of its promised reforms.

The Perception of Applying Pressure

Greece is in a tight spot and it has to find resolutions to two outstanding issues: the funding of its banking system, and the government’s liquidity situation. For the latter, the Greek government has more control. The markets saw that yesterday when Athens issued various decrees for local governments’ cash balances to be deposited at the central bank for the federal government’s use.

It’s the funding of the banking system that Greece has no control over. That’s dependent on the European Central Bank’s (ECB) role as the lender of last resort through the use of the eurozone’s Emergency Liquidity Assistance (ELA) program. The market now believes that ECB staff is preparing a proposal to subtly apply further pressure. The bank could do this by increasing haircuts on Greek bank collateral offered for ELA. The Eurogroup requires a Greek reaction, and as a member state, they are required to fulfill all protocols and not just back away from these responsibilities. Applying subtle pressure hopefully will garner a positive reaction. To date it has not and time is running out as the uncertainty over how Greece and its creditors will come to an agreement has led the market to continue to price in a Grexit. The Greek yield curve continues to invert (short yields rise faster than long ones would suggest default).

The question and answer yet to be discussed in detail is, “if a default and exit does become a reality, will the ECB’s quantitative easing program limit the contagion?”

German Sentiment Dented by Greek Crisis

German Sentiment Dented by Greek Crisis

The fall in German ZEW investor sentiment in April would suggest that fears over Greece are starting to dent confidence in Germany’s economic recovery. The fall in the headline economic sentiment indicator (53.3 versus 54.8) was the first in six months. Although the trend remains high, the headline decline follows this month’s fall in the German Sentix investor sentiment index, implying that the worsening Greek crisis is having an effect.

Data like this would suggest the possibility of Grexit could be a key threat to German business confidence and activity, no matter how large that economy is. Forex traders were short the EUR going into this morning’s event with market bids scattered well below (€1.0645-55).

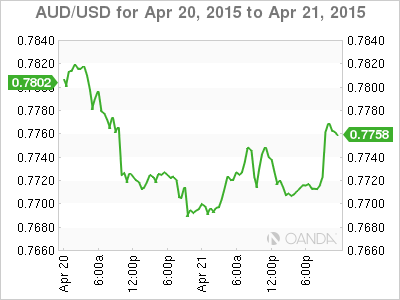

RBA Keeps the Door Ajar on Rates Cut

RBA Keeps the Door Ajar on Rates Cut

Governor Glenn Stevens and his fellow cohorts at the Reserve Bank of Australia (RBA) will probably stop at nothing to keep the Aussie from underperforming. Yesterday, Stevens reassured investors regarding the likelihood of further policy easing. His words appear to echo the latest RBA meeting minutes data that was released overnight.

The April RBA meeting was a rather close call in terms of how bank officials voted. Although a narrow majority favored to hold rates at +2.25%, the fixed-income dealers were very much onside for another rate cut. Nevertheless, the RBA minutes saw an advantage to wait for more data (a favorite stalling tactic at central banks), including the quarterly inflation figures due this evening for support in its decision. RBA officials added that household consumption and home building have picked up, but gross domestic product growth would likely remain below trend. Moreover, the central bank saw non-mining business investment as softer-than-expected, with the possibility of continued decline this year. The RBA did acknowledge that excessively low rates risk the fueling of housing market imbalances.

Stronger commodity prices supported the AUD above $0.78 for a brief period. The currency has since slipped; temporarily visiting sub-$0.77 after the minutes were released in the overnight session. The currency pair moves remain choppy with liquidity not as strong as to be expected. For the time being, the commodity- and interest rate-sensitive currency is expected to struggle under the pressure from high frequency selling interest, and too many long retail interest long AUD at bad levels.

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

{kind=link}